Managing money often feels complicated, especially when income must stretch across many priorities. The 50/30/20 rule offers a simple framework that breaks spending into clear categories without requiring complex calculations. Popular among financial educators, the approach focuses on balance rather than restriction. By dividing income into needs, wants, and savings, the rule provides structure while still allowing flexibility. Understanding how the 50/30/20 rule works can help frame everyday financial decisions in a more organized and intentional way.

What the 50/30/20 Rule Means

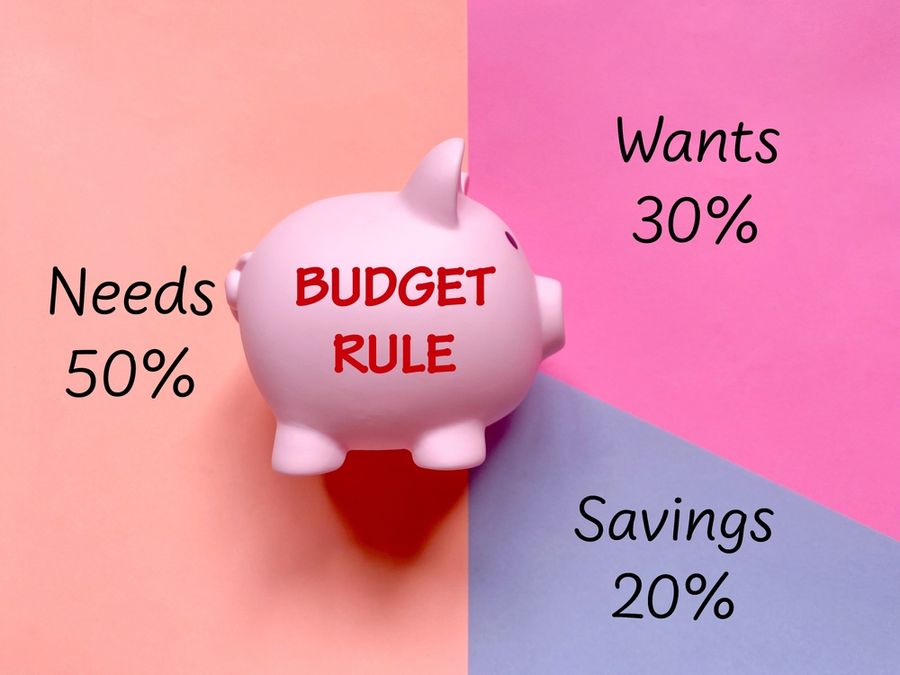

The 50/30/20 rule is a budgeting concept that divides after-tax income into three main categories. Fifty percent is allocated to essential expenses, thirty percent is reserved for discretionary spending, and twenty percent is directed toward savings or financial goals. The goal is to create a balanced approach that accounts for both obligations and personal enjoyment while still prioritizing future stability.

Rather than focusing on strict limits for every expense, the rule emphasizes proportions. Housing, utilities, groceries, and transportation usually fall under essential costs. Discretionary spending includes non-essentials such as entertainment, dining out, and hobbies. Savings typically cover emergency funds, retirement contributions, and other long-term financial priorities.

Understanding the “50” for Essential Expenses

The largest portion of the 50/30/20 framework is dedicated to essential expenses. Essential costs generally include bills that must be paid to maintain basic living standards. Rent or mortgage payments, utilities, insurance, transportation, and groceries are common examples. Minimum debt payments are often included because failing to pay them can lead to financial consequences.

Spending more than half of income on essentials is common in high-cost areas or during certain life stages. The rule serves as a reference point rather than a rigid standard. Reviewing essential expenses can highlight areas where costs may be fixed or difficult to change. Understanding how much income goes toward necessities can provide clarity around overall financial capacity and spending flexibility.

How the “30” Covers Discretionary Spending

The thirty percent portion of the rule is reserved for discretionary spending, sometimes referred to as lifestyle spending. Discretionary expenses are non-essential purchases that add comfort or enjoyment. Examples often include streaming services, dining out, travel, hobbies, and personal shopping. While not required for basic living, discretionary spending plays an important role in quality of life.

Separating discretionary expenses from essential costs can help clarify priorities. The rule does not suggest eliminating enjoyment but rather placing boundaries around it. Spending less than thirty percent on discretionary items may allow additional room for savings or debt reduction. Spending more can signal a need to reevaluate lifestyle choices.

The Role of the “20” for Savings and Financial Goals

The final portion of the rule focuses on savings and future-oriented financial goals. Twenty percent of income is commonly directed toward emergency savings, retirement accounts, and other long-term objectives. Savings can also include additional debt payments beyond required minimums. The emphasis is on building financial security over time.

Savings goals vary depending on individual circumstances. Some people prioritize emergency funds, while others focus on retirement or education savings. The rule encourages consistent progress rather than perfection. Allocating a defined portion of income toward savings helps make future planning a regular habit.

Why the 50/30/20 Rule Appeals to Many People

One reason the 50/30/20 rule remains popular is its simplicity. The structure avoids detailed line-item budgeting and focuses instead on broader spending patterns. Many people find the rule easier to maintain because it does not require tracking every transaction. The flexibility allows adjustments based on personal preferences and financial circumstances.

Another appeal lies in balance. The rule recognizes the importance of meeting obligations, enjoying income, and preparing for the future. It avoids extremes by allowing room for discretionary spending while still emphasizing savings. Financial educators often reference the rule as a starting point rather than a final solution.

A Simple Framework for Ongoing Money Awareness

The 50/30/20 rule provides a clear way to view income without adding unnecessary complexity. By organizing spending into three broad categories, the framework encourages intentional money management. It supports awareness of where income goes while leaving room for personal choice and lifestyle variation.

Financial habits evolve over time, and budgeting approaches often change alongside them. The 50/30/20 rule offers a starting structure that can be adjusted as needs shift. Whether followed closely or loosely, the framework highlights the importance of balancing obligations, enjoyment, and preparation for the future. Consistent awareness of income allocation remains a valuable tool for long-term financial stability.